- The US House previously passed a farm bill that includes a very large US$187 billion reduction to SNAP, alongside updates to crop insurance and commodity price supports that could reshape food assistance and agricultural markets for companies like Conagra Brands.

- At the same time, Conagra’s new Citizenship Report and updated bylaws highlight its focus on sustainability and shareholder engagement just as major policy changes introduce fresh demand uncertainty.

- We’ll now examine how this very large SNAP funding cut could influence Conagra’s investment narrative and perceived earnings resilience.

Outshine the giants: these 16 early-stage AI stocks could fund your retirement.

Conagra Brands Investment Narrative Recap

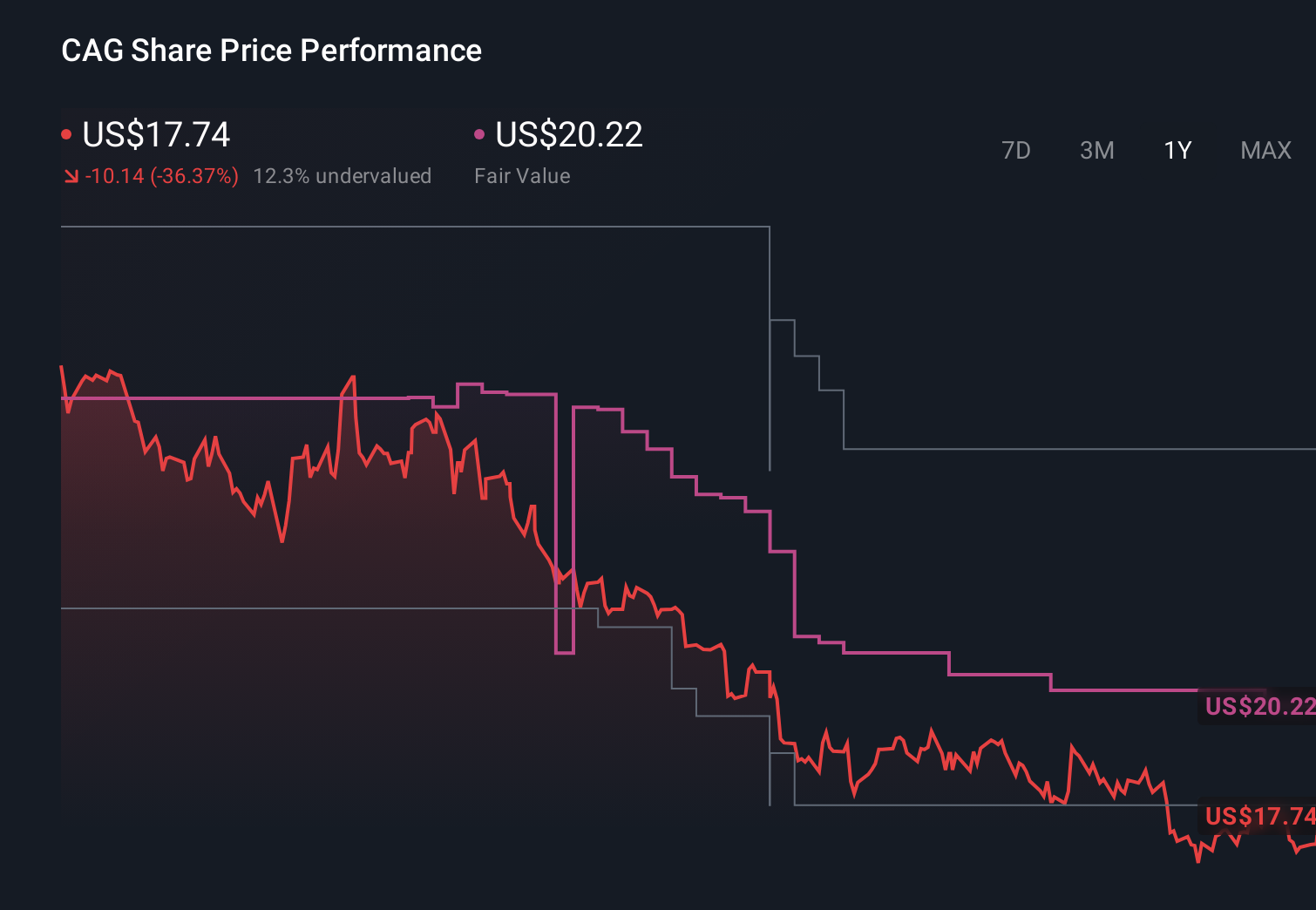

To own Conagra Brands, you need to believe its broad packaged and frozen portfolio can keep volumes and pricing relatively steady despite cost pressures and changing consumer habits. The very large US$187 billion SNAP cut heightens near term demand risk for value focused brands, while the key short term catalyst remains any evidence that Conagra can protect margins and stabilize volumes after a year of weak share price performance.

The most relevant recent update is Conagra’s Fiscal 2025 Citizenship Report, which outlines progress on food safety, waste reduction and climate targets. While it does not offset the near term demand risk from SNAP cuts, it speaks to how Conagra is trying to strengthen its operating profile and brand equity, which could influence how investors weigh earnings resilience against policy driven volume pressures.

Yet in contrast, investors should also be aware that the biggest near term risk may lie in how SNAP cuts interact with already pressured margins and…

Read the full narrative on Conagra Brands (it’s free!)

Conagra Brands’ narrative projects $11.4 billion revenue and $905.9 million earnings by 2028. This implies a 0.5% yearly revenue decline and an earnings decrease of about $300 million from $1.2 billion today.

Uncover how Conagra Brands’ forecasts yield a $18.75 fair value, a 31% upside to its current price.

Exploring Other Perspectives

Some of the lowest ranked analysts already expected flat revenue around US$11.2 billion and earnings of roughly US$1.1 billion by 2029, highlighting how differently you might view the SNAP cuts and shifting consumer preferences compared with the more optimistic consensus.

Explore 10 other fair value estimates on Conagra Brands – why the stock might be worth over 3x more than the current price!

Reach Your Own Conclusion

Don’t just follow the ticker – dig into the data and build a conviction that’s truly your own.

Searching For A Fresh Perspective?

Markets shift fast. These stocks won’t stay hidden for long. Get the list while it matters:

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be…

Read More: Large SNAP Cuts and Policy Shifts Might Change The Case For Investing In