The U.S. labor market in 2025 is navigating a delicate balance between resilience and moderation. While the unemployment rate remains near historic lows at 4.0% to 4.4%, job creation has slowed to an average of 104,000 per month—half the pace seen in late 2023—signaling a “healthy slowdown” as the economy adjusts to post-pandemic norms [1]. This transition, however, is not uniform: sectors like healthcare and education are thriving, while manufacturing and wholesale trade face headwinds. For investors, this divergence presents both risks and opportunities, demanding a strategic reallocation of capital in a cooling economy.

Labor Market Trends: A Tale of Two Sectors

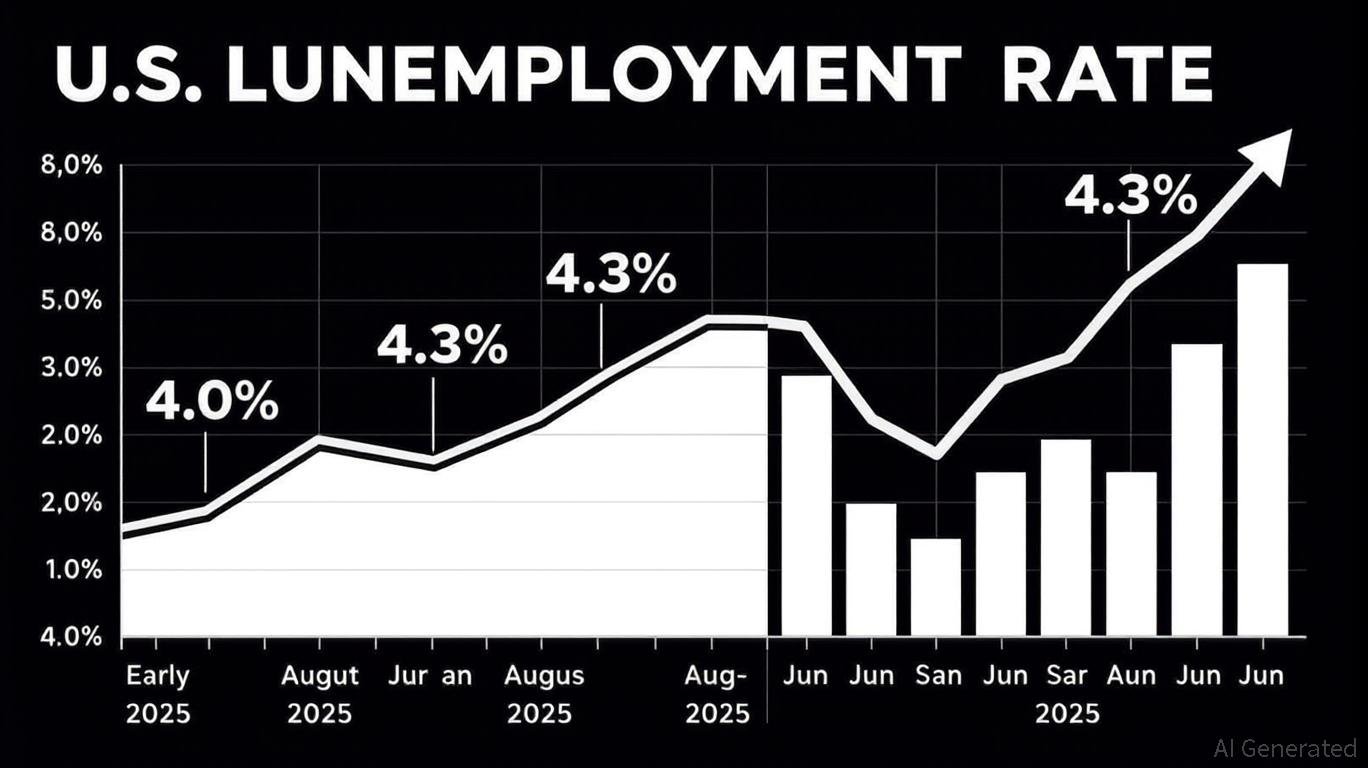

The labor market’s softening is most evident in the August 2025 jobs report, which revealed a mere 22,000 nonfarm payrolls added—far below the projected 75,000—and an unemployment rate of 4.3%, the highest since 2021 [2]. This marked a stark contrast to the robust hiring seen in 2023 and early 2024. Sector-specific data highlights the uneven recovery: healthcare added 31,000 jobs in August alone, while manufacturing and wholesale trade each lost 12,000 positions [2]. The latter’s struggles are partly attributable to President Trump’s April 2025 tariff announcements, which have exacerbated labor shortages and supply chain disruptions in manufacturing, leading to a cumulative loss of 78,000 jobs since April [5].

Meanwhile, wage growth has stabilized, with the Employment Cost Index (ECI) rising 3.6% year-over-year through June 2025, slightly outpacing the 2.7% CPI inflation rate [3]. Real wage growth across OECD countries averaged 2.5%, suggesting a modest but meaningful improvement in purchasing power [4]. Employers are increasingly prioritizing retention over recruitment, adopting skills-first strategies and internal development programs to mitigate turnover [2]. This shift underscores a broader trend: the labor market is evolving from a seller’s to a more balanced landscape, with implications for both corporate strategies and investor portfolios.

Equity Sector Implications: Tech and Consumer Discretionary Shine

The labor market’s slowdown has intensified expectations of Federal Reserve rate cuts, with markets pricing in a near-certain reduction in September 2025 [3]. This has triggered a realignment in equity sectors. Technology stocks, which benefit from lower discount rates on future earnings, surged following the August jobs report, with companies like Broadcom (AVGO) and Tesla (TSLA) posting double-digit gains [5]. Consumer discretionary and real estate sectors also appear well-positioned, as reduced borrowing costs could stimulate spending on big-ticket items and make homeownership more affordable [3].

Conversely, financials—particularly commercial banks—face headwinds. Compressed net interest margins loom as a risk if the Fed cuts lending rates faster than deposit rates [3]. Similarly, industrials and energy sectors underperformed in late August…

Read More: The Healthy Slowdown in the Labor Market and Its Implications for Equity